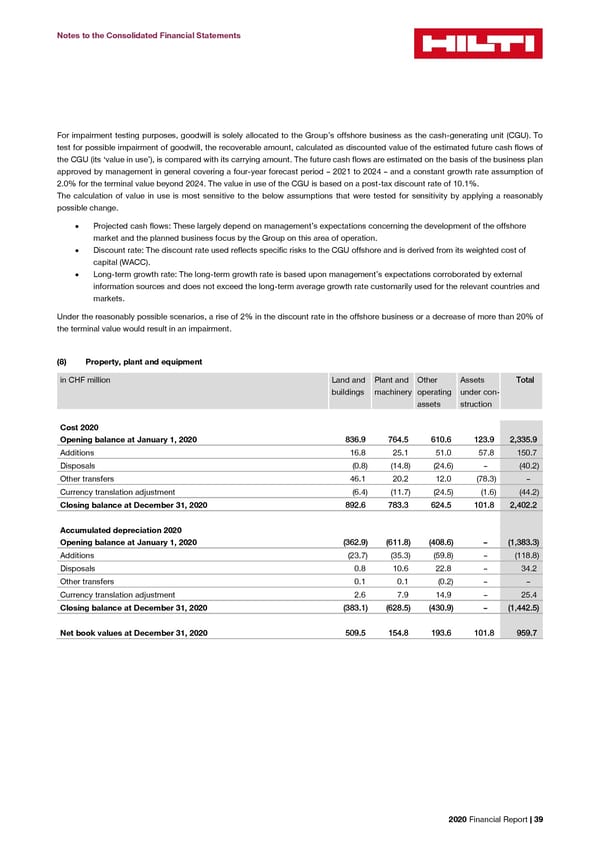

Notes to the Consolidated Financial Statements For impairment testing purposes, goodwill is solely allocated to the Group’s offshore business as the cash-generating unit (CGU). To test for possible impairment of goodwill, the recoverable amount, calculated as discounted value of the estimated future cash flows of the CGU (its ‘value in use’), is compared with its carrying amount. The future cash flows are estimated on the basis of the business plan approved by management in general covering a four-year forecast period – 2021 to 2024 – and a constant growth rate assumption of 2.0% for the terminal value beyond 2024. The value in use of the CGU is based on a post-tax discount rate of 10.1%. The calculation of value in use is most sensitive to the below assumptions that were tested for sensitivity by applying a reasonably possible change. • Projected cash flows: These largely depend on management’s expectations concerning the development of the offshore market and the planned business focus by the Group on this area of operation. • Discount rate: The discount rate used reflects specific risks to the CGU offshore and is derived from its weighted cost of capital (WACC). • Long-term growth rate: The long-term growth rate is based upon management’s expectations corroborated by external information sources and does not exceed the long-term average growth rate customarily used for the relevant countries and markets. Under the reasonably possible scenarios, a rise of 2% in the discount rate in the offshore business or a decrease of more than 20% of the terminal value would result in an impairment. (8) Property, plant and equipment in CHF million Land and Plant and Other Assets TToottaall buildings machinery operating under con- assets struction Cost 2020 Opening balance at January 1, 2020 883366..99 776644..55 661100..66 112233..99 22,,333355..99 Additions 16.8 25.1 51.0 57.8 150.7 Disposals (0.8) (14.8) (24.6) – (40.2) Other transfers 46.1 20.2 12.0 (78.3) – Currency translation adjustment (6.4) (11.7) (24.5) (1.6) (44.2) Closing balance at December 31, 2020 889922..66 778833..33 662244..55 110011..88 22,,440022..22 Accumulated depreciation 2020 Opening balance at January 1, 2020 ((336622..99)) ((661111..88)) ((440088..66)) –– ((11,,338833..33)) Additions (23.7) (35.3) (59.8) – (118.8) Disposals 0.8 10.6 22.8 – 34.2 Other transfers 0.1 0.1 (0.2) – – Currency translation adjustment 2.6 7.9 14.9 – 25.4 Closing balance at December 31, 2020 ((338833..11)) ((662288..55)) ((443300..99)) –– ((11,,444422..55)) Net book values at December 31, 2020 550099..55 115544..88 119933..66 110011..88 995599..77 2020 Financial Report | 39

2020 Financial Report Page 40 Page 42

2020 Financial Report Page 40 Page 42