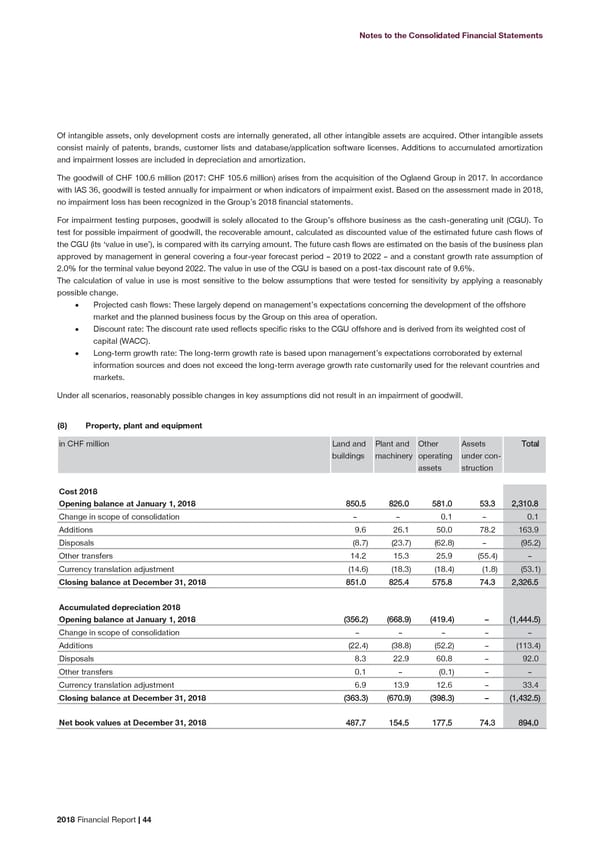

Notes to the Consolidated Financial Statements Of intangible assets, only development costs are internally generated, all other intangible assets are acquired. Other intangible assets consist mainly of patents, brands, customer lists and database/application software licenses. Additions to accumulated amortization and impairment losses are included in depreciation and amortization. The goodwill of CHF 100.6 million (2017: CHF 105.6 million) arises from the acquisition of the Oglaend Group in 2017. In accordance with IAS 36, goodwill is tested annually for impairment or when indicators of impairment exist. Based on the assessment made in 2018, no impairment loss has been recognized in the Group’s 2018 financial statements. For impairment testing purposes, goodwill is solely allocated to the Group’s offshore business as the cash-generating unit (CGU). To test for possible impairment of goodwill, the recoverable amount, calculated as discounted value of the estimated future cash flows of the CGU (its ‘value in use’), is compared with its carrying amount. The future cash flows are estimated on the basis of the business plan approved by management in general covering a four-year forecast period – 2019 to 2022 – and a constant growth rate assumption of 2.0% for the terminal value beyond 2022. The value in use of the CGU is based on a post-tax discount rate of 9.6%. The calculation of value in use is most sensitive to the below assumptions that were tested for sensitivity by applying a reasonably possible change. • Projected cash flows: These largely depend on management’s expectations concerning the development of the offshore market and the planned business focus by the Group on this area of operation. • Discount rate: The discount rate used reflects specific risks to the CGU offshore and is derived from its weighted cost of capital (WACC). • Long-term growth rate: The long-term growth rate is based upon management’s expectations corroborated by external information sources and does not exceed the long-term average growth rate customarily used for the relevant countries and markets. Under all scenarios, reasonably possible changes in key assumptions did not result in an impairment of goodwill. Property, plant and equipment (8) in CHF million Land and Plant and Other Assets Total buildings machinery operating under con- assets struction Cost 2018 Opening balance at January 1, 2018 850.5 826.0 581.0 53.3 2,310.8 Change in scope of consolidation – – 0.1 – 0.1 Additions 9.6 26.1 50.0 78.2 163.9 Disposals (8.7) (23.7) (62.8) – (95.2) Other transfers 14.2 15.3 25.9 (55.4) – Currency translation adjustment (14.6) (18.3) (18.4) (1.8) (53.1) Closing balance at December 31, 2018 851.0 825.4 575.8 74.3 2,326.5 Accumulated depreciation 2018 Opening balance at January 1, 2018 (356.2) (668.9) (419.4) – (1,444.5) Change in scope of consolidation – – – – – Additions (22.4) (38.8) (52.2) – (113.4) Disposals 8.3 22.9 60.8 – 92.0 Other transfers 0.1 – (0.1) – – Currency translation adjustment 6.9 13.9 12.6 – 33.4 Closing balance at December 31, 2018 (363.3) (670.9) (398.3) – (1,432.5) Net book values at December 31, 2018 487.7 154.5 177.5 74.3 894.0 2018 Financial Report | 44

2018 Financial Report Page 45 Page 47

2018 Financial Report Page 45 Page 47